XBRL is a language for the electronic communication of business and financial data which is revolutionising business reporting around the world. It provides major benefits in the preparation, analysis and communication of business information. It offers cost savings, greater efficiency and improved accuracy and reliability to all those involved in supplying or using financial data. It is an open standard, free of licence fees, being developed by a non-profit making international consortium. Other pages on this web site provide detailed information on XBRL, its technical features and its business opportunities.

XBRL can be applied to a very wide range of business and financial data. Among other things, it can handle:-

- Company internal and external financial reporting.

- Business reporting to all types of regulators, including tax and financial authorities, central banks and governments.

- Filing of loan reports and applications; credit risk assessments.

- Exchange of information between government departments or between other institutions, such as central banks.

- Authoritative accounting literature – providing a standard way of describing accounting documents provided by authoritative bodies.

All types of organisations can use XBRL to save costs and improve efficiency in handling business and financial information. Because XBRL is extensible and flexible, it can be adapted to a wide variety of different requirements. All participants in the financial information supply chain can benefit, whether they are preparers, transmitters or users of business data.

XBRL is set to become the standard way of recording, storing and transmitting business financial information. It is capable of use throughout the world, whatever the language of the country concerned, for a wide variety of business purposes. It will deliver major cost savings and gains in efficiency, improving processes in companies, governments and other organisations.

XBRL is being developed by an international non-profit consortium of major companies, organisations and government agencies. These include the world’s leading accounting, technology, government and financial services bodies.

XBRL increases the usability of financial statement information. The need to re-key financial data for analytical and other purposes can be eliminated. By presenting its statements in XBRL, a company can benefit investors and raise its profile. It will also meet the requirements of regulators, lenders and others consumers of financial information, who are increasingly demanding reporting in XBRL. This will improve business relations and lead to a range of benefits.

With full adoption of XBRL, companies can automate data collection. For example, data from different company divisions with different accounting systems can be assembled quickly, cheaply and efficiently. Once data is gathered in XBRL, different types of reports using varying subsets of the data can be produced with minimum effort. A company finance division, for example, could quickly and reliably generate internal management reports, financial statements for publication, tax and other regulatory filings, as well as credit reports for lenders. Not only can data handling be automated, removing time-consuming, error-prone processes, but the data can be checked by software for accuracy.

With full adoption of XBRL, companies can automate data collection. For example, data from different company divisions with different accounting systems can be assembled quickly, cheaply and efficiently. Once data is gathered in XBRL, different types of reports using varying subsets of the data can be produced with minimum effort. A company finance division, for example, could quickly and reliably generate internal management reports, financial statements for publication, tax and other regulatory filings, as well as credit reports for lenders. Not only can data handling be automated, removing time-consuming, error-prone processes, but the data can be checked by software for accuracy.

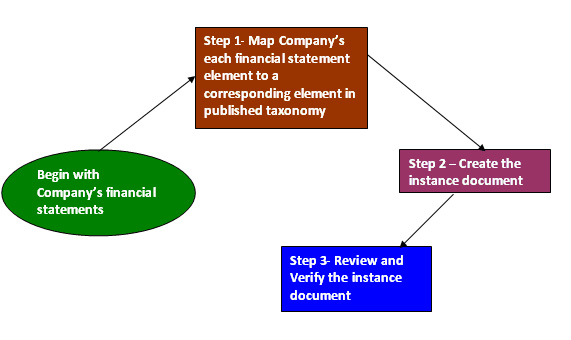

- XBRL-aware accounting software products are becoming available which will support the export of data in XBRL form. These tools allow users to map charts of accounts and other structures to XBRL tags.

- Statements can be mapped into XBRL using XBRL software tools designed for this purpose.

- Data from accounting databases can be extracted in XBRL format. It is not strictly necessary for an accounting software vendor to use XBRL; third party products can achieve the transformation of the data to XBRL.

- Applications can transform data in particular formats into XBRL. For example, web sites are in operation that can transform filings into XBRL format

The route which an individual company may take will depend on its requirements and the accounting software and systems it currently uses, among other factors.

Several software vendors are developing such tools in India and the companies are free to choose the one that suits them to create XBRL document.

A core purpose of Accounting Institutes around the world is to enhance the access, quality and breadth of financial information available to the investing public. XBRL will help achieve this. Institutes also believe that the development of XBRL will help position their members as valued knowledge providers for their clients. Businesses, large and small, are undergoing fundamental change. Accountants, as the managers of the underlying language of business, can help organisations fit into the new digital world, solve business issues and capitilise on opportunities.

No. XBRL is simply a language for transmitting information. It must accurately reflect data reported under different standards – it does not change them.

XBRL benefits comparability by helping to identify data which is genuinely alike and distinguishing information which is not comparable.

Technical FAQs

The value of the xlink:href attribute in the schemaRef element in the instance document must be http://www.mca.gov.in/XBRL/2011/05/25/Taxonomy/CnI/ci/in-gaap-ci-2011-03-31.xsd.

HTML (Hypertext Markup Language) is a standard way of marking up a document so it can be published on the World Wide Web and viewed in a browser. It provides a set of pre-defined tags describe on how content appears in a browser. For example, it describes the font and colour of text. It gives little information on meaning or context. XML (Extensible Markup Language) uses tags to identify the meaning, context and structure of data.

XML is a standard language which is maintained by the World Wide Web Consortium (W3C). XML does not replace HTML; it is a complementary format that is platform independent, allowing XML data to be rendered on any device such as a computer, cell phone, PDA or tablet device. It enables rich, structured data to be delivered in a standard, consistent way. Whereas HTML offers a fixed, pre-defined number of tags, XML neither defines nor limits tags. Instead, XML provides a framework for defining tags (i.e. taxonomy) and the relationship between them (i.e. schema).

XBRL is an XML-based schema that focuses specifically on the requirements of business reporting. XBRL builds upon XML, allowing accountants and regulatory bodies to identify items that are unique to the business reporting environment. The XBRL schema defines how to create XBRL documents and XBRL taxonomies, providing users with a set of business information tags that allows users to identify business information in a consistent way. XBRL is also extensible in that users are able to create their own XBRL taxonomies that define and describe tags unique to a given environment.

XML is a standard language which is maintained by the World Wide Web Consortium (W3C). XML does not replace HTML; it is a complementary format that is platform independent, allowing XML data to be rendered on any device such as a computer, cell phone, PDA or tablet device. It enables rich, structured data to be delivered in a standard, consistent way. Whereas HTML offers a fixed, pre-defined number of tags, XML neither defines nor limits tags. Instead, XML provides a framework for defining tags (i.e. taxonomy) and the relationship between them (i.e. schema).

XBRL is an XML-based schema that focuses specifically on the requirements of business reporting. XBRL builds upon XML, allowing accountants and regulatory bodies to identify items that are unique to the business reporting environment. The XBRL schema defines how to create XBRL documents and XBRL taxonomies, providing users with a set of business information tags that allows users to identify business information in a consistent way. XBRL is also extensible in that users are able to create their own XBRL taxonomies that define and describe tags unique to a given environment.

Many of the pages constitute the XML Schemas defining XBRL, and the change log. In the remaining pages, there are many more examples, fragments included from the defining schemas, greater detail about pre-existing XBRL 2.0 features, and detailed explanations of the new features.

There have always been restrictions on what is a meaningful taxonomy schema, meaningful linkbase, and meaningful instances. In the past many of these criteria were implicit; these criteria are now part of the specification. In some cases, they may be enforced using XML Schema, requiring no new code to be written, and in other cases the specification enables vendors to write correct validation code. Examples of these technical enhancements include: a detailed exposition of handling variable precision numbers, prohibitions on certain kinds of loops in relationships, and prohibition of duplicated data in instances. The meaning of calculation links and their ability to express relationships between items in different tuples has been specified precisely.

Domain experts and application developers can now encode more precise information about financial reporting concepts in XBRL taxonomies. They can also define the handling of new relationships not defined by XBRL itself. New relationships allow taxonomy authors to connect taxonomy definitions to authoritative definitions and other supporting documentation.

Yes, we expect taxonomy authors gradually to upgrade their taxonomies to 2.1. This is a prerequisite for conformance with the Financial Reporting Taxonomies Architecture (FRTA) 1.0. However, 2.0 versions of these taxonomies may also be made available at the discretion of the taxonomy authors.

The conformance suite consists of over 250 example taxonomy fragments (XML Schema and XLink files) and instance documents, containing both valid and invalid usage. It will help application developers ensure their software processes XBRL correctly.

The XBRL International Domain Working Group developed a detailed set of requirements which were then implemented by the XBRL International Specification Working Group.

The XBRL 2.1 Conformance Suite is posted in a large (more than 5MB) zip file on the XBRL International web site, alongside the XBRL 2.1 specification. The Conformance Suite contains over 250 separate XBRL instances. Although the instances are small, there is a subset of them that are specifically designed to exercise each feature of an XBRL instance and their interactions.

XBRL is a format for exchanging information between applications. Therefore each application will store data in whatever form is most effective for its own requirements and import and export information in XBRL format so that it can be readily imported or exported in turn by other applications. In some applications, for example, the XBRL formatted information being used may be mostly tabular numeric information, hence easily manipulated in a relational database. In other applications, the XBRL information may consist of narrative document-like structures with a lot of text, so that a native XML database may be more appropriate. There is no mandatory relationship between XBRL and any particular database or other processing or storage architecture.

MCA Specific FAQs

XBRL instance document creation software has to be purchased from the software vendors in the market. This software is used to create XBRL instance documents that would be uploaded on the MCA portal. MCA21 system shall provide a facility for validation of the instance document and filing of the same. MCA is not recommending any specific XBRL software.

ICAI, which is assisting MCA with conduct of XBRL training, has been instructed to develop standard Training module as well identify resource persons in consultation with XBRL training partners located at different parts on the country. It is proposed to engage leading chambers of industry and other professional institutes, namely, ICWAI and ICSI in future trainings. Training will be held over the next few months in most leading cities of India. Details of the same will be available on our website www.mca.gov.in/www.xbrl.icai.org.

Existing Form 23AC and 23ACA shall continue to be there for filing by companies to which XBRL filing is not applicable; and for filing of earlier year’s documents.

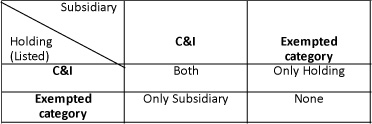

Subsidiary of listed company is required to file in XBRL format, irrespective of its paid up capital.

XBRL is a collection of standardized, machine-readable “tags” for line items in financial statements, including footnotes and schedules. It is similar in concept to bar codes used to identify products. Using XBRL, each line in a financial statement is assigned a standardized data tag.

XBRL is a standards-based way to communicate business and financial information. These communications are defined by metadata set out in taxonomies. Taxonomies capture the definition of individual reporting concepts as well as the relationships between concepts and other semantic meaning.

The taxonomy comprises of the following components:-

XBRL is a standards-based way to communicate business and financial information. These communications are defined by metadata set out in taxonomies. Taxonomies capture the definition of individual reporting concepts as well as the relationships between concepts and other semantic meaning.

The taxonomy comprises of the following components:-

- Schema – Defines the elements used in the linkbases

- Presentation linkbase – Which defines the structure for displaying the data, along with the preferred label attribute.

- Calculation linkbase – Establishes the arithmetical relationship of simple addition and subtraction, which is done by way of a weight attribute (1 or -1)

- Label linkbase – Stores the labels about the concepts (it is the human readable name of the element)

The XML and XSDs actually make the real taxonomy. The excel sheet is just for you to view it. An XBRL processor (a computer software that understands and/or manipulates XBRL documents) will need those XML and XSD documents.

XBRL is a standards-based way to communicate business and financial information. These communications are defined by metadata set out in taxonomies. Taxonomies capture the definition of individual reporting concepts as well as the relationships between concepts and other semantic meaning.

Questions from Stakeholders

The companies whose Balance Sheet date is 31.03.2011 or onwards, need to file their financial statements in XBRL provided they qualify the criteria laid as per Ministry’s general Circular 37/2011 dated 07.06.2011.

The holding company has to file consolidated financial statement in XBRL. Its subsidiaries also need to file their financials in XBRL.

If the Subsidiary company meets the criteria of phase-I category of companies, they have to file in the XBRL mode.

All such companies, whose financial statements are generated as per accounting requirements other than Schedule VI of the Company Act, 1956 have been exempted from XBRL filing for year 2010-11. The companies regulated by any other act like Electricity Act, 2003, Banking Regulation Act, 1949, Insurance Act, etc are exempted from XBRL filing in the Phase-I filings. Similarly, companies registered as a NBFC have been exempted from XBRL filing for year 2010-11.

The certification of XBRL filing would be done by the professional as before. The professional may use XBRL viewer tool to satisfy himself about the authenticity of XBRL document as per the audited financial statements.

Yes, all the subsidiaries (including subsidiary of a subsidiary of a listed company) of a listed company in India need to file their financial statements in XBRL this year.

Applicability of XBRL filing would as under